In the financial sector, record keeping is usually crucial to both the consumer, as well as the company. Another method of ensuring that organizations maintain accuracy of their financial management is through Bank Reconciliation Bank Statement. Here we shall discuss what Bank Reconciliation Bank Statement are, why they should be done, how they should be done and why understanding them is important for every business or individual who intends to run a successful and solvent financial organization.

What is Bank Statement Reconciliation?

Bank statement reconciliation is the elaborate exercise of matching your records of the transactions with the recorded ones on the bank statement. The main goal is to check that the records match and if there i are differences displayed. When disparities surface, reconciliation plays the role of helping to define their source and to correct them.

When explaining what is bank statement reconciliation getting to it, we can define it as a critical process that ensures the finance impressive of any organizational finance statement is accurate. Reconciliations carried out on a frequent basis can reduce errors and bad management, which should improve one’s financial state.

Importance of Bank Statement Reconciliation

- Error Detection: Omissions can occur when recording accounting information, sometimes it may be a typographical error, or a transaction may have been missed. Such errors are easy to discover during regular reconciliations.

- Fraud Prevention: many people keep monitoring their bank statements in order to notice unauthorized transactions. It means that if there is something on your statement that you do not remember or never heard of, it might be an act of fraud.

- Budget Management: Reconciliation means you are able to see where you are spending your money to the last penny. It will also enhance budgeting and financial planning because one is in a position to understand how better to organize their finances.

- Financial Reporting: Reconciliation allows an organization to give a correct picture of its financial status, which is an important aspect in the preparation of reports especially for business organizations.

Understanding Reconciliation in Banks

Similar to account holders, reconciliation in banks is not only essential for practice but is significant for the banks as well. In the current work context, the reconciliations are conducted by banks themselves as a way to check whether the records in their systems match the records of their customers. This activity entails reconciling the information on post-executed transactions with the balances in different accounts.

Understanding reconciliation in banks is essential for several reasons:

- Accuracy: Checking that records generated by the bank tally with the records generating customers assures the financial figures’ credibility.

- Customer Trust: When banks do their records reconciliation frequently, the customers are also assured of their financial transactions which are well managed.

- Compliance: Reconciliation becomes compliance when regulation authorities demand that financial institutions keep records that are accurate.

What is Reconciliation of Bank Statement?

When you hear what is reconciliation of bank statement it means the procedure of comparing entries entered in your own accounting records with records appearing in your bank statement. This is an important step when trying to manage your financial needs well.

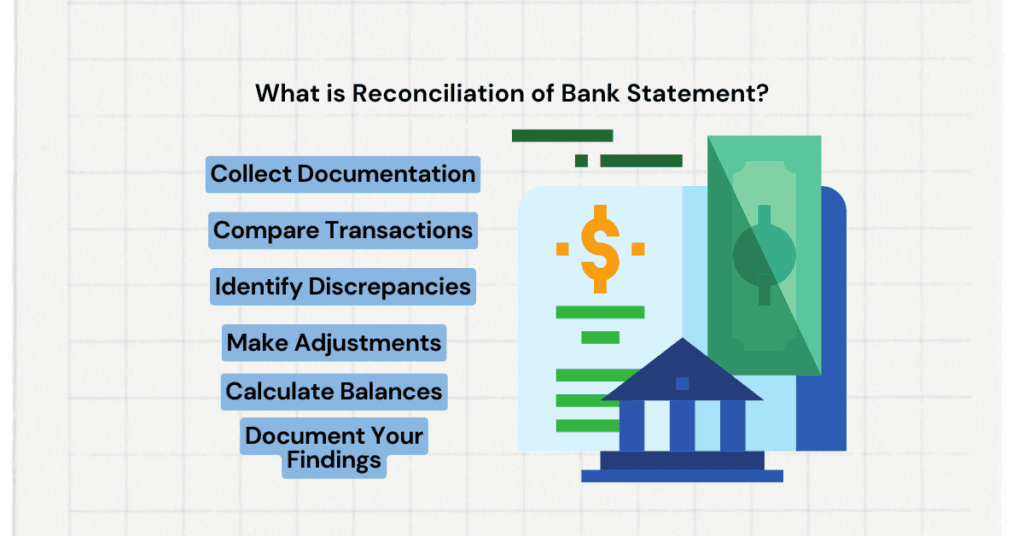

Six steps in Reconciling a Bank Statement

- Collect Documentation: To begin is to secure your bank statement and your financials that are personal or/and business.

- Compare Transactions: From the listed bank statement, review every transaction in your statement and try to match with your records. Circle those transactions that are similar.

- Identify Discrepancies: Make sure to indicate any transaction in this table that does not correspond with the other. This may include checks not recorded, bank charges or interest to be written.

- Make Adjustments: The following steps need to be taken: Enter the transactions that went unnoticed earlier, in your business records.

- Calculate Balances: After adding up all the adjustments you need to check whether your calculated ending balance is the same as the ending balance given on the bank statement.

- Document Your Findings: Always make a note of your reconciliation for future use. This is especially the case in the course of an audit or when the company is receiving a financial review.

Bank Statement Bank Reconciliation

The term bank statement bank reconciliation stresses the symbiotic relationship between Bank statements and reconciliation process. The systematic approach is important to follow when you want to reconcile your bank statement.

Advantage of Bank statement bank Reconciliation

- Improved Financial Clarity: This way, you are able to know your financial situation hence easy to understand and manage the cash flows.

- Error Correction: Checking regularly is preventive in that it can always solve some mistakes before they become huge issues.

- Preparation for Audits: Reconciliations must be done regularly and this allows for a correct record in case auditors or any financial assessment companies decide to perrform an audit.

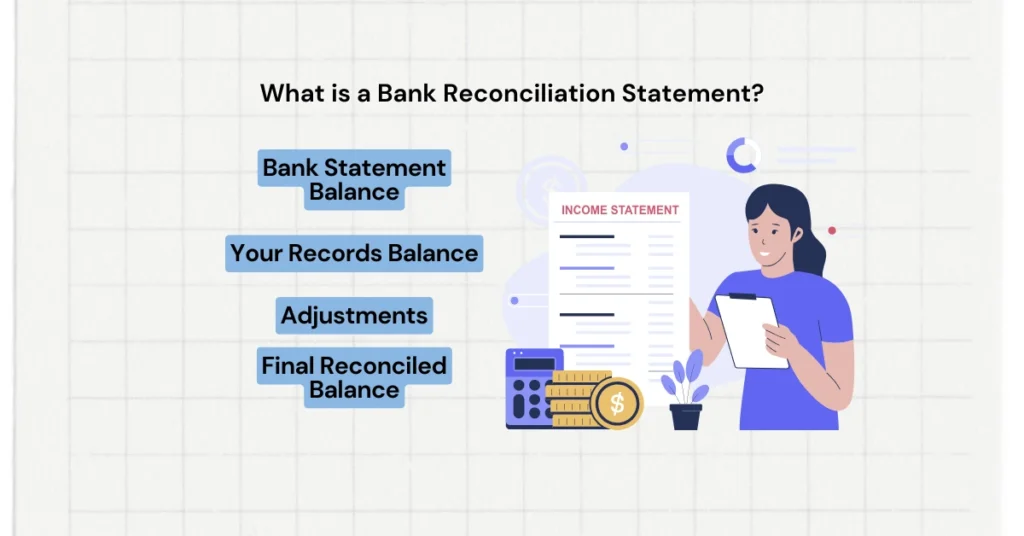

What is a Bank Reconciliation Statement?

A bank reconciliation statement is a statement that shows the differences between your bank statement and your book totals. This statement contains any variations proven at the time when performing the reconciliation.

Components of a Bank Reconciliation Statement

When someone asks what is a bank reconciliation statement, the document typically includes:

- Bank Statement Balance: The balance given at the end of your bank statement.

- Your Records Balance: The balance obtained from the actual accounting records of the enterprise.

- Adjustments: A list of all the corrections that were made as well those extra additions manufactured when performing the reconciliation.

- Final Reconciled Balance: The position arrived at after all adjustments in an account have been made.

Also Read | Maximize Your Earnings: Learn the Profit and Loss Formula for Smarter Decisions!

How to Create a Bank Reconciliation Statement

Creating a bank reconciliation statement involves:

- Starting with the Bank Statement Balance: Start with the balance brought forward from the last bank statement you prepared.

- Adjust for Outstanding Transactions: Include any payments paid to the supplier but not yet debited on his account and deduct any cheques still outstanding.

- Adjust for Bank Fees: This encouraged me to note and write off any bank charges that I that were not recorded.

- Verify Adjusted Balance: C Annual adjustments should be made after properly checking that the balance matches one’s account after all the necessary correction.

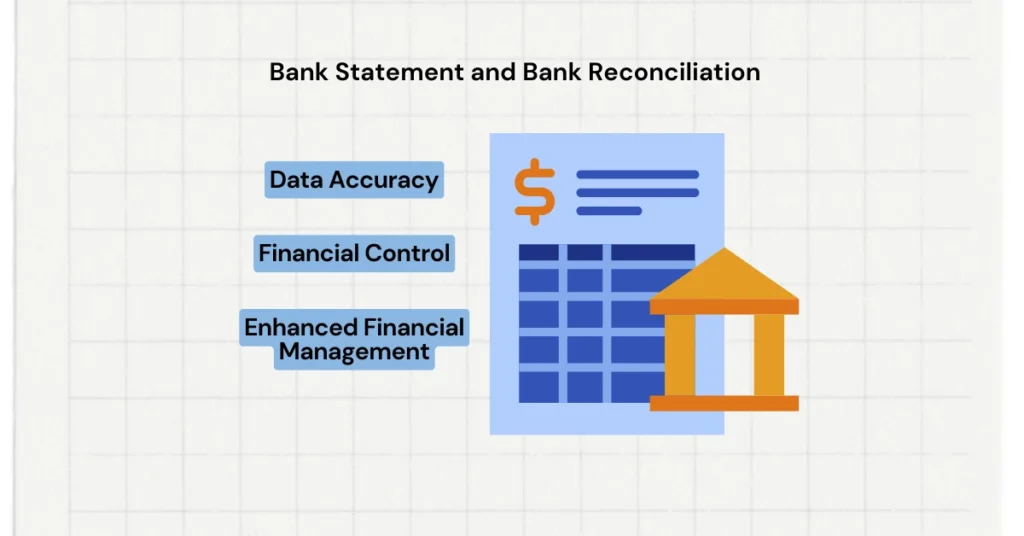

Bank Statement and Bank Reconciliation

It is impossible to overemphasize the relationship between the bank statement and the bank reconciliation. The bank statement contains the information required to complete the reconciliation process and the reconciliation process in turn enables one to check the correctness of the information found in the bank statement.

The Relationship between Bank Statements and Reconciliation

- Data Accuracy: A bank statement is a record of these transactions and reconciliation is the process of verifying that information is consistent with your records.

- Financial Control: Compiling your ledger against your bank statement often enables one to have control over his/her financial position so as to make appropriate changes.

- Enhanced Financial Management: This relationship facilitates in issuance of sound financial decisions since spending habits and cash flow trends are explained.

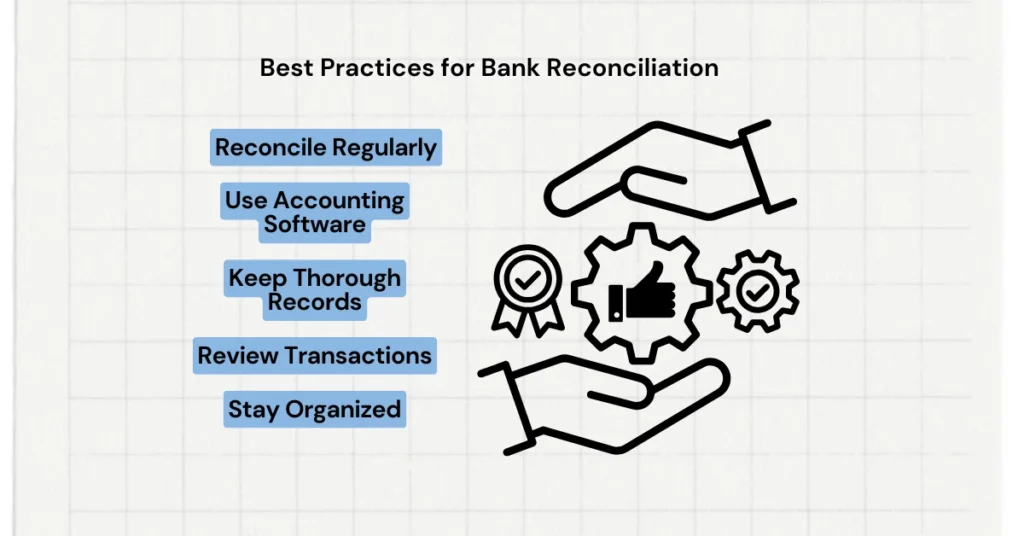

Best Practices for Bank Reconciliation

To effectively implement a bank reconciliation bank statement process, consider the following best practices:

- Reconcile Regularly: It is wise to balance your bank statements on a monthly basis. This frequency assist in detecting such errors early and is important to guarantee the records are correct as possible.

- Use Accounting Software: Utilize accounting software to minimize or completely eliminate manual reconciliation, should the software already have one in place.

- Keep Thorough Records: It is advisable to retain original receipts and invoices to facilitate reconciliation so that all records of the transaction should be kept proper.

- Review Transactions: Run daily transactions through, with a view of identifying any transactions that seem out of place or in some way fraudulent.

- Stay Organized: Set up a special flow of documents for subsequent storing to provide an optimized process of their reconciliation.

Conclusion

An important part of managing personal or company finances properly is familiarizing oneself with bank reconciliation bank statements. Therefore understanding what reconciliation is, its importance in banks and how to prepare a bank reconciliation statement is crucial as it refines ones financial management skills and avails one from frequent errors.

BothChecking and Rechecking promptly enables one to get it right in his business, especially when making decisions on projects, preparing financial statements, and in cases of taxes. Adopt these, in that case, and you will be on your way to progressing towards improved financial position.

Therefore, whenever you get your bank statement, make sure you do a extra ordinary reconciliation process. You will be thanking your future self for the mindful preparation sometime in the future!